Forms & Documents

Access Essential Forms and Documents to Streamline the Non-QM Financing Process

Find All Your Required Forms & Documents Here

Our comprehensive library of forms and documents is designed to provide you with everything you need to navigate the lending process efficiently and confidently. Whether you’re a TPO mortgage broker or a business owner, you’ll find organized, easy-to-access resources tailored to your unique financing needs.

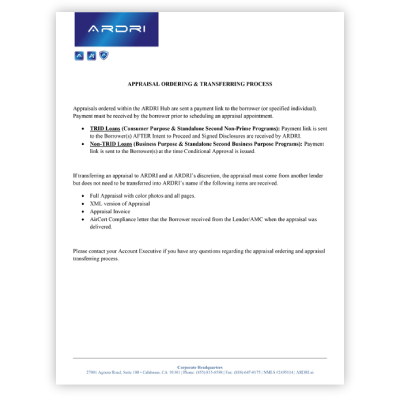

This job aid provides step-by-step guidance for TPO MLOs and Processors on how to manually order appraisals through ARDRI’s Mercury Network portal. It outlines how to log in or create credentials, complete the appraisal order form for both Consumer and Business Purpose loans, and properly select required options such as AMC assignment and appraisal form…

The Borrower Certification and Authorization Certification confirms that the borrower has provided accurate and complete information in their mortgage application and acknowledges the lender’s right to verify details through a full documentation review.

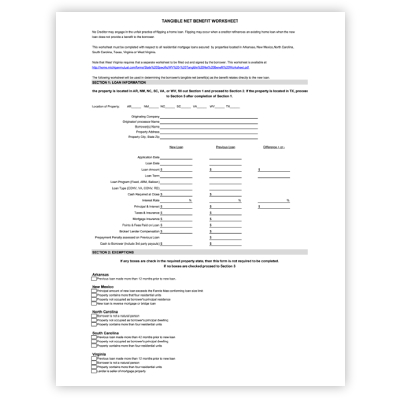

To help us deliver fast, reliable turn-times and close your Business Purpose loans in 30 days or less, ARDRI requires a set of Minimum Submission Requirements for the initial underwrite and disclosure process. These items ensure your file enters our workflow complete, accurate, and aligned with our published SLAs—so you and your borrowers experience a…

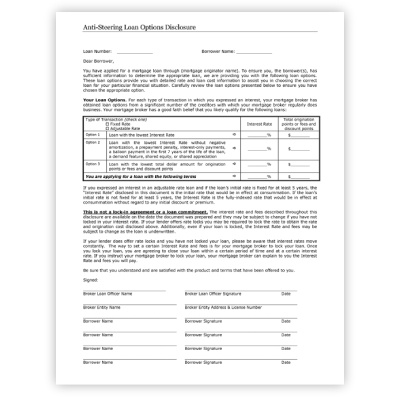

The Business Purpose Anti-Steering Letter is a compliance document that certifies a mortgage loan was originated for business or investment purposes, rather than consumer use. This letter helps ensure that borrowers were not improperly directed toward a specific loan product for the benefit of the lender or broker.

To support fast, compliant, and efficient processing, ARDRI requires specific Minimum Submission Requirements for all Consumer Purpose loans. These items ensure your file is complete for initial underwrite and disclosures, helping us meet our published SLAs and consistently close loans in 30 days or less.

Required and must be approved by ARDRI for all Third Party Origination firms wanting to earn Lender Paid Compensation. Once approved, the pricing and eligibility engine will reflect Lender Paid Pricing automatically within the loan premium and Par pricing when selecting Borrower Paid Compensation.

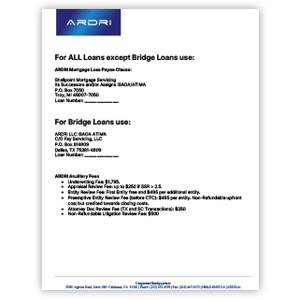

The Mortgage Loss Payee Clause is a provision in a property insurance policy that designates the lender (mortgagee) as the payee in the event of a loss. It provides security for the lender by guaranteeing that insurance proceeds will be used to repair or rebuild the property or to satisfy outstanding loan obligations in case…

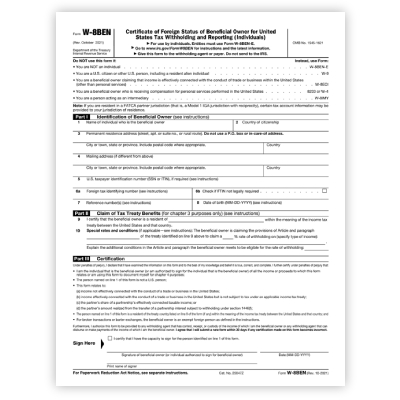

This form is required under Section 440 of Article 12-A of the New York Real Property Law for all mortgage transactions involving ARDRI in the state of New York. It serves as a legal attestation by the referring party or broker confirming that the referenced mortgage loan is not a consumer-purpose loan under Section §590…

To help us deliver fast, reliable turn-times and close your Business Purpose loans in 30 days or less, ARDRI requires a set of Minimum Submission Requirements for the initial underwrite and disclosure process. These items ensure your file enters our workflow complete, accurate, and aligned with our published SLAs—so you and your borrowers experience a…

The Business Purpose Anti-Steering Letter is a compliance document that certifies a mortgage loan was originated for business or investment purposes, rather than consumer use. This letter helps ensure that borrowers were not improperly directed toward a specific loan product for the benefit of the lender or broker.

This form is required under Section 440 of Article 12-A of the New York Real Property Law for all mortgage transactions involving ARDRI in the state of New York. It serves as a legal attestation by the referring party or broker confirming that the referenced mortgage loan is not a consumer-purpose loan under Section §590…

This document outlines the requirements, disclosures, and contractual terms for Third Party Originators (TPOs) seeking approval to submit Business Purpose loans to ARDRI. It details the TPO application process, required company documentation, broker responsibilities, compliance and fraud prevention standards, underwriting and closing roles, compensation structure, and ongoing representations and warranties.

This document outlines the application requirements, disclosures, and contractual framework for Third Party Originators (TPOs) seeking approval to submit both consumer and business purpose loans to ARDRI. It details required company information and documentation, broker duties and compliance obligations, fraud prevention standards, and AML/BSA requirements.

The Mortgage Loss Payee Clause is a provision in a property insurance policy that designates the lender (mortgagee) as the payee in the event of a loss. It provides security for the lender by guaranteeing that insurance proceeds will be used to repair or rebuild the property or to satisfy outstanding loan obligations in case…

To support fast, compliant, and efficient processing, ARDRI requires specific Minimum Submission Requirements for all Consumer Purpose loans. These items ensure your file is complete for initial underwrite and disclosures, helping us meet our published SLAs and consistently close loans in 30 days or less.

This document outlines the application requirements, disclosures, and contractual framework for Third Party Originators (TPOs) seeking approval to submit both consumer and business purpose loans to ARDRI. It details required company information and documentation, broker duties and compliance obligations, fraud prevention standards, and AML/BSA requirements.

This job aid provides step-by-step guidance for TPO MLOs and Processors on how to manually order appraisals through ARDRI’s Mercury Network portal. It outlines how to log in or create credentials, complete the appraisal order form for both Consumer and Business Purpose loans, and properly select required options such as AMC assignment and appraisal form…

The Borrower Certification and Authorization Certification confirms that the borrower has provided accurate and complete information in their mortgage application and acknowledges the lender’s right to verify details through a full documentation review.

Required and must be approved by ARDRI for all Third Party Origination firms wanting to earn Lender Paid Compensation. Once approved, the pricing and eligibility engine will reflect Lender Paid Pricing automatically within the loan premium and Par pricing when selecting Borrower Paid Compensation.

The Mortgage Loss Payee Clause is a provision in a property insurance policy that designates the lender (mortgagee) as the payee in the event of a loss. It provides security for the lender by guaranteeing that insurance proceeds will be used to repair or rebuild the property or to satisfy outstanding loan obligations in case…

The Roster of Mortgage Loan Originators and Loan Processors spreadsheet allows brokers to input and add their employees to the ARDRI Hub. This helps ensure that all relevant team members are accurately registered within the ARDRI platform for streamlined communication and tracking.

Simplify Your Path to Non-QM Success

Join the many TPO brokers who trust ARDRI for their Non-QM and Business Purpose financing needs. Becoming an approved broker is quick and hassle-free—no financial information or credit checks are required. Unlock innovative solutions and personalized support with ARDRI—your trusted partner in navigating the Non-QM financing landscape. Start today!

Call us today at 855.855.8598 to learn more or get approved below!